Estimated reading time: 15 minutes

In 2026, comprehensive car insurance in South Africa usually costs about R800 to R1,400 per month for many drivers, but your actual premium can be much lower or much higher depending on your age, claims history, car, suburb, mileage, excess, and cover level. Third-party only cover can start from around R70 per month, while high-risk drivers or expensive cars can push comprehensive premiums well past R2,000.

The important point is this: car insurance is priced around risk, not around a fixed market price. Once you understand what insurers are actually pricing, you can often bring your premium down without leaving yourself underinsured.

Key takeaways

- Most comprehensive car insurance premiums in South Africa sit in a broad middle range of roughly R800 to R1,400 per month.

- Younger drivers usually pay more, while experienced drivers with clean records often pay less.

- Your premium is heavily influenced by your car’s value, theft risk, where you live, where you park, how much you drive, and your claims profile.

- Comparing quotes, reviewing your policy yearly, adjusting your excess carefully, and updating your insurer when your risk changes are some of the fastest ways to save.

- The cheapest policy is not always the best value. Good cover at the right price matters more than the lowest monthly debit order.

What you’ll learn

This article explains what car insurance costs in South Africa in 2026, why prices vary so much, what insurers look at when they calculate your premium, and which changes can reduce your monthly cost without stripping out useful cover. You’ll also see how to think about excess, vehicle value, age, mileage, no-claim history, and the difference between cheap insurance and good-value insurance.

What does car insurance cost in South Africa in 2026?

For most drivers shopping for comprehensive cover, a realistic range is about R800 to R1,400 per month. That is the number many people want first, and it is useful as a benchmark, but it is only a starting point.

Across the wider market, pricing tends to break down like this:

| Cover type | Typical monthly range | What it usually covers |

|---|---|---|

| Third-party only | From around R70 to R500 | Damage you cause to others, not your own car |

| Third-party, fire and theft | About R200 to R700 | Third-party damage plus fire and theft on your car |

| Comprehensive | About R800 to R1,400 for many drivers, but can go much higher | Your car, third-party damage, theft, accidents, and other insured risks |

This explains why one driver might pay under R500 while another pays more than R2,000 for the same category of cover. The product name may look similar, but the risk profile behind it is completely different.

Why do car insurance premiums vary so much?

Car insurance prices vary because insurers are estimating the chance and cost of a future claim. They look at how likely you are to have an accident, how likely your car is to be stolen, how expensive it is to repair, and how large a payout could be if something goes wrong.

That means your premium is not random, and it is not personal in the emotional sense. It is personal in the data sense. If your profile suggests higher risk, you pay more. If it suggests lower risk, you pay less.

This is why two drivers with similar cars can still get very different quotes. One may have a longer claims-free record, park in a garage, drive fewer kilometres, live in a lower-risk suburb, and choose a higher excess. All of that changes the pricing model.

What do insurers actually look at when pricing your policy?

Insurers usually price your premium using three broad groups of factors: vehicle factors, driver factors, and cover factors.

Vehicle factors

Your car’s make, model, age, value, repair cost, parts availability, and theft profile matter a lot. A modest hatchback with cheaper parts and lower theft risk is usually cheaper to insure than a high-performance or luxury vehicle.

Your vehicle’s insurable value also matters. Terms like trade value, retail value, and book value often come up here. In simple terms, a higher-value vehicle creates a bigger possible payout for the insurer, so the premium is usually higher too. As your car depreciates over time, your premium should usually be reviewed so you are not still paying as if the car were worth much more than it is now.

Driver factors

Your age, driving experience, licence history, accident record, previous claims, and sometimes credit-related risk indicators can affect what you pay. Younger drivers usually pay more because they are statistically more likely to be involved in accidents. Drivers with a long, clean history usually get more favourable pricing.

Cover factors

The type of cover you choose changes everything. Comprehensive cover costs more because it protects more. Third-party only costs less because it leaves your own car out of the claim equation. Your excess also matters. A higher excess often lowers your monthly premium, while a lower excess pushes it up.

Add-ons can raise the price too. Car hire, tyre and rim cover, scratch and dent cover, roadside assistance, and similar extras may be useful, but they are not always worth carrying forever.

How much do younger drivers pay?

Age is one of the clearest cost drivers in South African car insurance. The broad trend is simple: younger drivers usually pay more, then premiums tend to settle as experience improves and the claims profile becomes more favourable.

A useful rough age breakdown from your source material looks like this:

| Age band | Average monthly premium |

|---|---|

| 18 to 25 | R1,672 |

| 26 to 29 | R1,542 |

| 30 to 35 | R1,325 |

| 36 to 39 | R1,188 |

Some of your notes also point to lower averages in older age groups, although pricing can still rise again later depending on the insurer and risk profile. The bigger takeaway is that age on its own is not the whole story. A careful 27-year-old with lower mileage and a modest car can still price better than an older driver with a poor claims history and a high-risk vehicle.

Does where you live affect your premium?

Yes, often more than people expect. Location is one of the quieter pricing factors, but it can be a major one. Insurers look at local crime, theft trends, traffic density, accident patterns, and even the difference between nearby suburbs.

That is why premiums can differ across provinces and within the same city. Your source material points to averages above R1,300 in places like Gauteng and Limpopo. Those numbers are less important than the principle behind them: neighbourhood risk matters, and where the car is kept overnight matters too. A car parked in a locked garage usually presents a lower risk than one kept on the street every night.

How does mileage change the price?

Mileage matters because it changes your exposure to risk. A car that spends more time on the road has more opportunities to be involved in an accident or loss event than a car used lightly for short local trips.

This matters even more now because some insurers reward low mileage or safe driving behaviour through usage-based or telematics-linked models. If you work from home, commute less than you used to, or drive only occasionally, that can be worth telling your insurer. A policy based on old driving habits can leave you paying for risk you no longer present.

Which mistakes make people overpay for car insurance?

A lot of overpaying comes from avoidable admin and decision mistakes, not just from a bad market price. The most common ones are surprisingly basic.

1. Not comparing quotes

This is still one of the biggest reasons people overpay. Insurers price risk differently, so two quotes for the same driver can be far apart. If you do not compare, you never really know whether your current premium is competitive.

2. Choosing the wrong cover type

Some people buy more cover than they need. Others slash cover too far and create a financial problem for themselves later. The right choice depends on the car’s value, your cash reserves, and how much loss you could realistically absorb yourself.

3. Ignoring the excess

A low excess makes claims easier to absorb, but it can also inflate the monthly premium. A carefully chosen higher excess can reduce monthly costs, but only if you could actually afford that amount in a real claim.

4. Forgetting to update the insurer

If you moved to a safer area, now work from home, reduced your mileage, or added a better security device, your insurer should know. If your risk went down and your policy stayed the same, you may be overpaying.

5. Claiming for every small incident

A claim can affect future pricing and any claims-free discount structure. That does not mean you should never claim. It means you should understand the long-term cost of small claims before submitting them.

6. Driving a high-risk vehicle

Repair costs, theft rates, and performance profile all affect premiums. Car insurance should be part of the buying decision before you sign for a vehicle, not only after.

7. Missing discounts and rewards

Some insurers reward lower mileage, good driving behaviour, bundled products, or loyalty. You do not always get these automatically. Sometimes you have to qualify, ask, or switch.

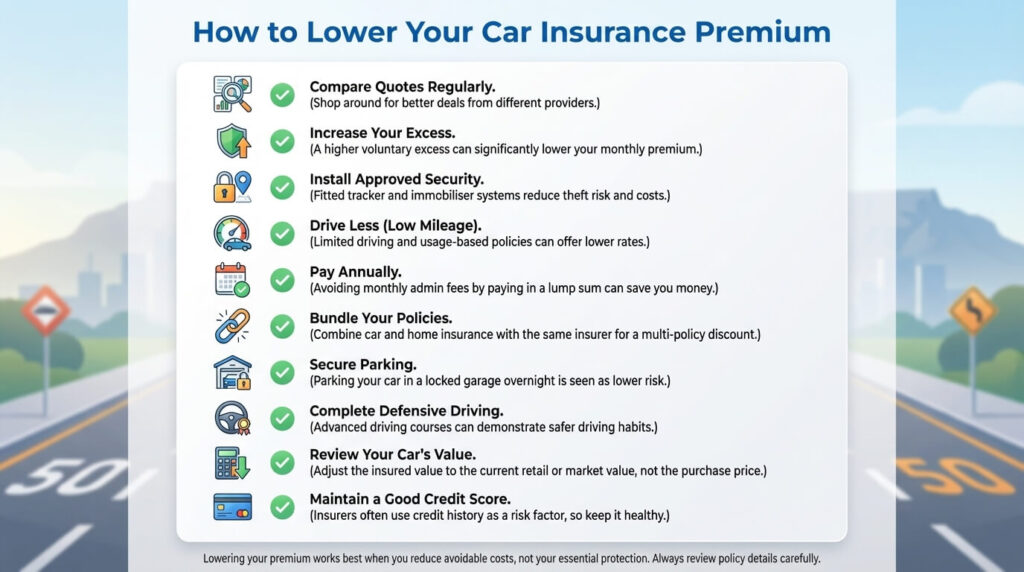

How can you lower your car insurance premium without losing cover?

This is where most articles go thin. The real answer is not “just find cheaper insurance”. It is to reduce unnecessary cost while protecting the parts of the policy that actually matter.

1. Compare quotes at least once a year

This is the simplest practical move. Do not assume your renewal quote is your best quote. Even if you stay with your current insurer, competitive quotes give you leverage and context.

2. Review your excess properly

A moderate increase in excess can lower your monthly premium. The trick is to find the level that you could still pay in a real claim without panic borrowing or dipping into money you do not have.

3. Remove add-ons you are not really using

Not every extra is bad, but not every extra deserves a permanent place on your schedule either. Review car hire, tyre and rim cover, scratch and dent cover, and roadside extras one by one.

4. Update your mileage and use case

If you drive less now than when you first took out the policy, say so. Lower annual mileage can support a lower premium.

5. Improve security where realistic

Alarm systems, immobilisers, tracking devices, and secure overnight parking can reduce theft risk and sometimes pricing. This is especially relevant for theft-prone vehicles or areas.

6. Protect your claims record where sensible

Not every minor bump has to become an insurance claim. Sometimes paying for a very small repair yourself is cheaper than the downstream pricing effect of another claim. This depends on the damage amount, your excess, and your current claims profile.

7. Review your cover as the car depreciates

As the vehicle’s value falls, your policy should still make sense for the current insurable value. A policy review every year helps prevent value drift.

8. Choose value, not just the lowest price

The cheapest premium can leave you with a painful excess, missing benefits, or cover gaps that only show up when something goes wrong. Better value usually means the policy is priced fairly for your actual needs, not stripped down to the point of regret.

9. Ask about discount structures

Depending on the insurer, you may find discounts linked to claims-free years, low mileage, bundled policies, or behaviour-based products.

10. Think about insurance before buying the next car

The cheapest car to buy is not always the cheapest car to insure. Insurance cost should sit next to fuel, maintenance, and finance when comparing vehicles.

What is the difference between cheap insurance and good-value insurance?

Cheap insurance is just low on price. Good-value insurance balances price, cover, exclusions, excesses, and claim usability.

That matters because it is easy to save R200 a month and lose far more later through a weak policy structure. Third-party only cover can be the right move for an old, low-value vehicle. It can also be a bad move if losing your own car would create a serious financial problem. In other words, the right policy is not only about what you can pay every month. It is also about what loss you could survive.

A useful way to think about this is to ask three questions:

- What would happen financially if my own car were written off tomorrow?

- Could I comfortably pay this excess if I had to claim next week?

- Am I paying for extras I would not miss if they disappeared?

Those questions usually expose whether you are optimising well or just chasing a lower debit order.

What role does excess play in total cost?

Your excess is the amount you pay yourself when you claim. A higher excess often lowers your monthly premium because you are taking on more of the claim burden yourself. A lower excess usually increases the premium because the insurer carries more of the claim cost.

There is no universal best setting. The right excess is one that saves you money month to month without becoming unaffordable during a claim. If your excess is set so high that you could not realistically pay it, the policy may look cheaper on paper but feel unusable when you need it most.

This is also why comparing policies on premium alone can mislead you. Two quotes can look close in price but be very different once you compare compulsory excesses, additional excesses, young driver excesses, or after-hours incident excesses. That is where a lot of “cheap” quotes stop looking cheap.

How should first-time buyers think about car insurance?

First-time buyers often get hit with the worst combination: limited claims history, limited driving history, tight budgets, and a strong urge to cut cost fast. That makes it easy to buy the wrong policy.

A better first-time buyer approach looks like this:

- Start by understanding the real difference between comprehensive, third-party fire and theft, and third-party only.

- Get multiple quotes before deciding what “normal” looks like for your profile.

- Ask what is actually included, not just what the premium is.

- Choose an excess you could genuinely pay.

- Keep your record clean where possible, because the first few claims-free years matter.

For many younger drivers, this is less about finding a miracle low premium and more about avoiding expensive mistakes that keep the premium high for longer.

How can you tell if you are overpaying right now?

You may be overpaying if any of the following is true:

- You have not compared quotes in more than 12 months.

- Your mileage has fallen but your policy still reflects old driving habits.

- Your car has depreciated, but your premium has not been reviewed.

- You are paying for extras you forgot about.

- You moved, changed parking arrangements, or improved security and never updated the insurer.

- Your excess is very low and your premium feels high.

- You are renewing automatically without checking whether your current policy still suits your risk.

These are not guarantees, but they are the right warning signs to investigate.

A simple action plan to cut your premium this month

If you want a practical next step, use this order:

- Pull your current policy schedule and renewal premium.

- Check your excesses, add-ons, and cover type.

- Confirm your vehicle value and whether the policy still matches it.

- Update your mileage, suburb, parking, and security details if anything changed.

- Compare at least three fresh quotes.

- Decide whether a slightly higher excess would still be affordable.

- Keep the cover that protects you from the losses you could not easily absorb yourself.

This is simple, but it is how a lot of real savings happen. The biggest gains often come from review and alignment, not from finding a gimmick.

Is car insurance still worth it if money is tight?

In many cases, yes. The monthly cost can feel painful, but being uninsured can be far more expensive if the car is stolen, written off, or badly damaged in an accident.

That does not automatically mean everyone needs comprehensive cover at all costs. It means some level of insurance protection is often worth keeping because the downside of being completely exposed is so high. The right level depends on your vehicle’s value, your budget, and whether you could replace or repair the car yourself if the worst happened.

A common range for many drivers in 2026 is about R800 to R1,400 per month, but high-risk profiles and expensive vehicles can push that much higher. Your actual quote depends on your risk profile, not just the cover label.

Third-party only is usually the cheapest option, sometimes starting from around R70 per month. It is cheaper because it does not cover damage to your own car.

High premiums are often driven by a mix of age, claims history, high-risk vehicle choice, where you live, where you park, mileage, cover level, and excess structure. It is usually a combination, not one single problem.

It often lowers the monthly premium, but it is only a good idea if you could still afford the excess during a claim. A cheap premium with an unaffordable excess can backfire.

At least once a year is a sensible baseline, and also whenever something meaningful changes, such as your mileage, address, parking setup, vehicle, or use pattern.

Summary

Car insurance cost in South Africa in 2026 is best understood as a range, not a fixed number. Many drivers land somewhere around R800 to R1,400 per month for comprehensive cover, while cheaper and more limited options sit well below that. What you pay depends on your own risk profile, especially your age, vehicle, suburb, mileage, claims record, excess, and cover choice.

The main opportunity is not to hunt blindly for the lowest premium. It is to make sure your policy still matches your real-world risk and needs. When you compare quotes, review your excess, update changed details, trim unnecessary extras, and choose cover with intention, you give yourself a much better chance of paying a fair price for the protection you actually need.

Want to see whether you’re paying too much for cover? Compare South African car insurance quotes through CoverMatch and check how your current premium stacks up against the market.

Last updated: